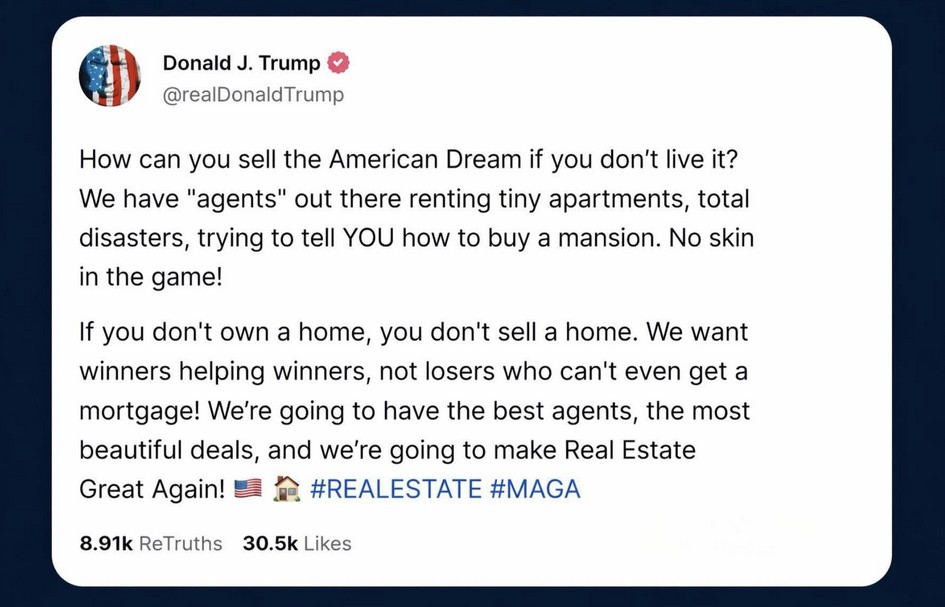

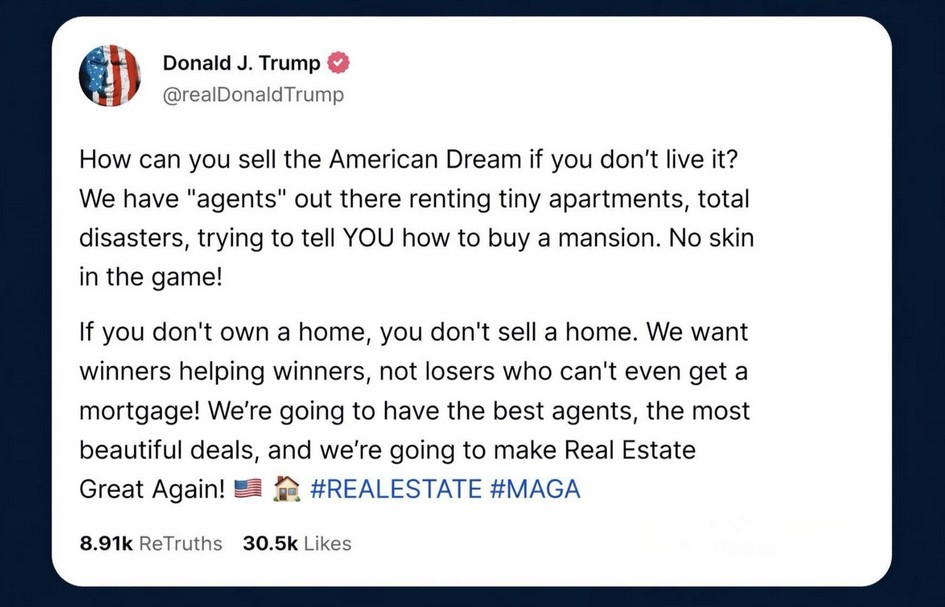

A screenshot attributed to President Donald Trump recently sparked a conversation that real estate has needed to have for a long time. The post argues that if you do not own a home, you should not be selling homes. It frames ownership as proof that an agent has “skin in the game,” and it questions whether someone who has never lived the American Dream can credibly sell it to someone else.

Chart note: The attached screenshot is used here as the reference point for the discussion. The broader issue is not one political post. The issue is whether the real estate industry has the right standards for who is allowed to guide consumers through the largest financial transaction of their lives.

Chart note: The attached screenshot is used here as the reference point for the discussion. The broader issue is not one political post. The issue is whether the real estate industry has the right standards for who is allowed to guide consumers through the largest financial transaction of their lives.

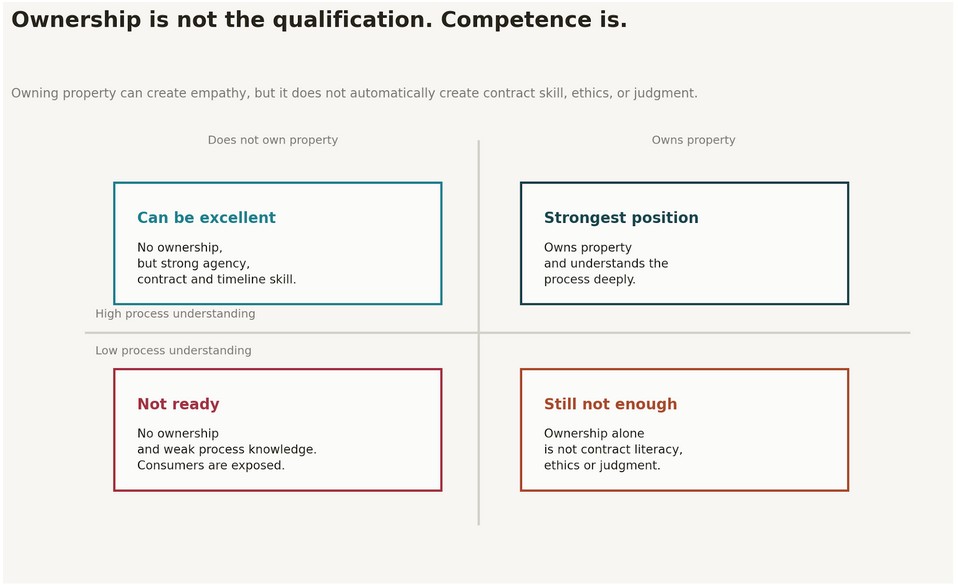

I disagree with the premise that you must own a home to sell one. That standard sounds tough, but it is the wrong test. A person can own property and still be careless, unethical, unprepared, bad with contracts, bad with people, and dangerous inside a transaction. Another person can rent, live with family, or be saving for their first home, and still deeply understand agency, financing, inspections, appraisals, deadlines, negotiation, disclosures, fair housing, contract language, and client risk.

Ownership can create empathy. It can make the process more personal. It can help an agent understand what it feels like to be on the other side of the table. But ownership does not automatically create competence.

The real standard should be this: if you are licensed to help someone buy or sell a home, you should understand the process at a professional level. You should be old enough to accept the responsibility of legal paperwork. You should be able to read the governing contracts. You should understand the consequences of mistakes. And you should respect the fact that for many families, this is not just a transaction. It is their largest asset, their savings, their future, and their peace of mind.

The Problem With the “You Must Own a Home” Argument

The argument that agents should have to own property comes from a real frustration. Consumers have met agents who talk confidently but do not understand the process. Buyers have been represented by agents who do not know how to explain financing. Sellers have worked with agents who cannot read a net sheet, understand inspection risk, or explain what happens if a buyer misses a deadline. The frustration is valid.

But the proposed solution is flawed.

Homeownership is not a professional qualification. It does not prove you know how to write an offer. It does not prove you understand the difference between inspection periods, financing contingencies, appraisal gaps, title defects, escrow deposits, seller credits, HOA disclosures, flood zones, condo documents, survey issues, lead-based paint disclosures, or post-closing occupancy agreements.

It also creates a fairness problem. If ownership became a requirement, the industry would shut out many of the exact people we claim to serve: young professionals, first-generation Americans, renters saving for a down payment, people in expensive cities, people recovering from financial setbacks, and people who may be excellent advocates precisely because they understand the struggle of getting into ownership.

The National Association of Realtors reported that first-time buyers fell to a historic low share of 21% of all buyers in its 2025 Profile of Home Buyers and Sellers, while the typical first-time buyer age rose to 40 (National Association of Realtors). If the typical first-time buyer is now 40, then requiring agents to own property before practicing would punish younger professionals for the same affordability crisis they are trying to help clients navigate.

That does not raise the bar. It narrows the door.

Chart note: The point is not that ownership has no value. The point is that ownership is not the same as competence. The strongest agent may be someone who owns property and understands the process, but a renter with deep process knowledge can be far safer for consumers than a homeowner with weak professional judgment.

The Bar Should Be Higher, But It Should Be the Right Bar

The real issue is not whether an agent owns a home. The issue is whether the licensing system proves enough.

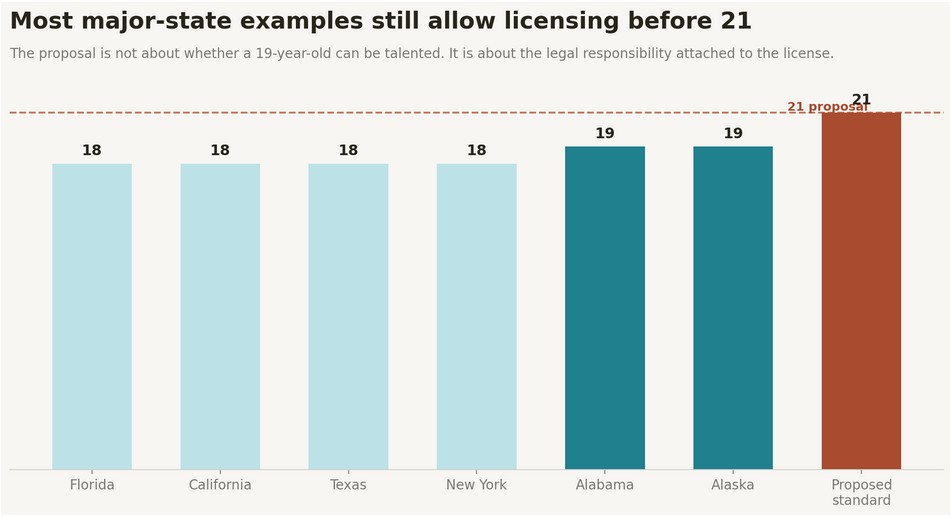

In many major states, a person can become licensed at 18. Florida requires sales associate applicants to be at least 18 and have a high school diploma, with post-license education and continuing education after licensure (Florida DBPR). California requires salesperson applicants to be 18 or older, honest and truthful, and to complete three college-level real estate courses before qualifying for the license process (California Department of Real Estate). Texas requires sales agent applicants to be at least 18, meet qualifications for honesty, trustworthiness, and integrity, complete 180 hours of qualifying education, pass the exam, clear fingerprints and background requirements, and be sponsored by a broker before performing real estate services (Texas Real Estate Commission). New York requires applicants to be 18, complete 77 hours of approved qualifying education, pass the state exam, and be sponsored by a New York licensed broker (New York Department of State).

Some states already go slightly higher. Alabama requires applicants to be at least 19 years old for license issuance documentation (Alabama Administrative Code). Alaska also requires real estate salesperson applicants to be at least 19 and work for a licensed broker, while also imposing criminal-history restrictions tied to competent and safe practice (Alaska Real Estate Commission).

My opinion is that the minimum age to hold a real estate license in this country should be 21.

Not because every 21-year-old is more mature than every 18- or 19-year-old. That is not true. There are 18-year-olds with discipline, professionalism, and work ethic that some 40-year-olds still do not have. Age alone does not create character.

But real estate agents are not just opening doors. They are helping write and fill in legal documents. They are explaining deadlines that can cost people deposits. They are advising families on decisions that may affect their financial life for years. They are handling negotiations where one wrong sentence can create confusion, conflict, or liability.

An 18-year-old can vote. An 18-year-old can work. An 18-year-old can serve. But that does not mean every regulated profession should open at 18 when the job involves contract preparation, fiduciary duties, consumer risk, and the movement of major household wealth.

Chart note: The 21-year-old standard would be a higher threshold than the current rule in many large states. Florida, California, Texas, and New York allow licensing at 18; Alabama and Alaska set the threshold at 19 (Florida DBPR, California Department of Real Estate, Texas Real Estate Commission, New York Department of State, Alabama Administrative Code, Alaska Real Estate Commission).

Chart note: The 21-year-old standard would be a higher threshold than the current rule in many large states. Florida, California, Texas, and New York allow licensing at 18; Alabama and Alaska set the threshold at 19 (Florida DBPR, California Department of Real Estate, Texas Real Estate Commission, New York Department of State, Alabama Administrative Code, Alaska Real Estate Commission).

The Contract-Language Issue Nobody Wants to Say Out Loud

There is another part of this conversation that will make people uncomfortable, but it needs to be said carefully and clearly.

I speak Spanish. I am of Spanish descent. I believe Spanish-speaking consumers deserve representation, respect, and access. I believe bilingual agents are essential in this country. I believe a buyer should be able to ask questions in the language they understand best, especially when that buyer is making the biggest purchase of their life.

But I also believe that if the contract is written in English, the licensed professional handling that contract must be able to read and understand English at the level required to explain what is being signed.

That is not anti-Spanish. That is consumer protection.

California’s salesperson exam content explicitly includes “appropriate knowledge of the English language, including reading, writing, and spelling,” along with knowledge of contracts, agency, fiduciary duties, conveyancing documents, and the legal effect of real estate instruments (California Department of Real Estate). That is the point. If the governing documents are in English, English contract literacy is not optional.

This matters because real estate documents are not casual reading. They are dense, technical, and legal. A contract deadline is not a suggestion. An inspection clause is not a decoration. A financing contingency is not just a paragraph. If an agent cannot read the controlling language, the consumer is exposed.

The Consumer Financial Protection Bureau has warned that limited English proficient consumers face barriers completing applications and contracts, understanding financial documents, resolving problems with financial products, and accessing financial education materials (Consumer Financial Protection Bureau). The CFPB also reported that most financial institutions it interviewed said written contracts or agreements were available only in English, and that successful translation of financial terms requires language fluency, cultural competency, and financial expertise (Consumer Financial Protection Bureau).

That last phrase matters: language fluency, cultural competency, and financial expertise. One without the others is not enough.

The Opposing View: Language Access Is Not a Loophole. It Is a Civil and Economic Necessity. There is a strong argument against making all real estate school and testing English-only. That argument deserves to be taken seriously.

The United States has millions of consumers who speak a language other than English at home. The CFPB reported that more than 65 million people, about 21% of the U.S. population over age five, speak a language other than English at home, and roughly two-fifths of that group have limited English proficiency (Consumer Financial Protection Bureau). Spanish is the most common non-English language, and Spanish, Chinese, Vietnamese, Korean, and Tagalog speakers account for more than 78% of limited-English-proficient individuals in the CFPB’s cited data (Consumer Financial Protection Bureau).

If the industry makes licensing harder for bilingual applicants, it could reduce access for communities that already face barriers. The National Association of Realtors has highlighted the importance of bilingual and culturally competent professionals in serving Hispanic homebuyers, noting that language gaps can expose consumers to predatory or misunderstood terms, including mortgage terms that buyers did not understand (National Association of Realtors). NAR also reported that Hispanic homeownership has reached 51%, with nearly 10 million Hispanic homeowning households, making homeownership a major wealth-building tool for Hispanic families (National Association of Realtors).

That is the counterargument: if Spanish-speaking buyers need Spanish-speaking agents, then Spanish-language education and testing may expand access, increase representation, and help consumers work with professionals who understand their language and culture.

Pennsylvania recently moved in that direction. The Pennsylvania Department of State announced that real estate sales and broker licensing exams and study guides became available in Spanish beginning November 1, 2025, as part of a stated effort to remove barriers to professional licensure and maximize accessibility by allowing applicants to test in their native language (Pennsylvania Department of State). Florida’s DBPR-developed examinations are available in English and Spanish at no additional cost, while national examinations are available only in English, and applicants may petition for other native-language exams under specific conditions (Florida DBPR).

That is not a small point. The opposing view says: do not confuse consumer protection with gatekeeping. Do not make English-only licensing a barrier that keeps qualified bilingual professionals out. Do not punish agents who can serve communities that English-only agents often cannot serve well.

That argument has weight.

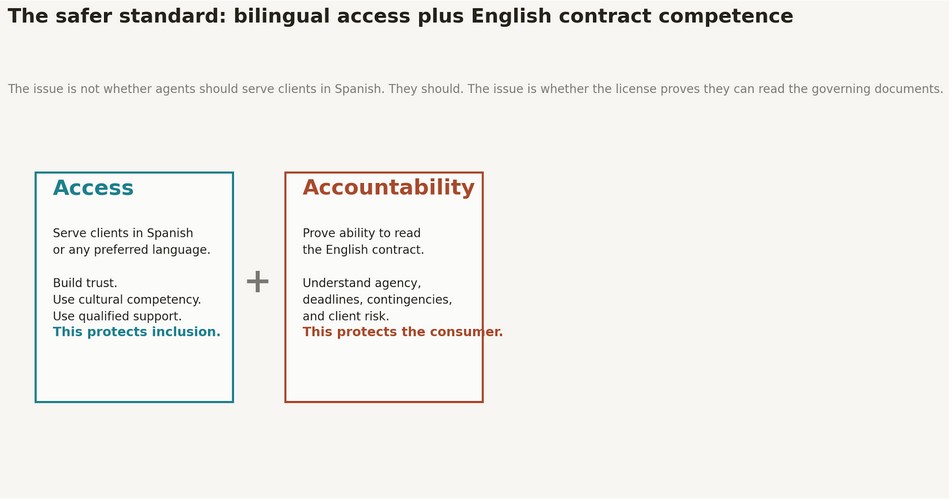

My Position: Bilingual Access, Yes. English Contract Competency, Also Yes.

The solution is not to remove Spanish from the real estate industry. That would be wrong, unrealistic, and harmful.

The solution is to separate client service language from governing contract competence.

Agents should absolutely be able to serve clients in Spanish. Schools should be able to provide Spanish-language support. Brokerages should train agents to serve limited-English-proficient consumers with professionalism and respect. Translated summaries, glossaries, interpreters, and bilingual education resources can help consumers understand the process.

But the license should still prove that the agent can read and understand the English-language contracts that govern the transaction.

NAR advises real estate professionals serving non-English-speaking clients to consider third-party translators, use written interpreter or translator agreements, avoid relying blindly on automated translation tools, and make sure clients understand that translations are provided to facilitate understanding while the English-language documents govern the transaction (National Association of Realtors). That is the balanced standard: serve the client in the language they understand, but do not pretend the legal document says something the agent cannot read.

This is where my view may sound strict, but it is rooted in responsibility. If all the contracts used in a state are written in English, then the testing process should include a meaningful English contract-comprehension requirement. Not conversational English. Not memorized vocabulary. Actual contract comprehension.

That is not the same as saying Spanish-speaking agents do not belong. I am saying the opposite. Spanish-speaking agents belong, and they are needed. But when the agent is the professional guiding a client through English legal documents, the agent must be able to understand those documents.

Chart note: The safer standard is not access or accountability. It is both. A real estate industry that serves Spanish-speaking consumers well should welcome bilingual service while requiring English contract competence when English contracts control the transaction.

Competence Is an Ethics Issue

This is not only about age or language. It is about competence.

The NAR Code of Ethics is built around honesty, fairness, professionalism, cooperation in clients’ best interests, and duties to clients and customers (National Association of Realtors). NAR also notes that Realtors must complete ethics training every three years and that the Code spells out professional responsibilities for members (National Association of Realtors).

Ethics without competence is not enough. Good intentions do not fix a missed deadline. A nice personality does not cure a badly written offer. A social media following does not explain a financing contingency. A rented apartment does not disqualify an agent, and owning a house does not qualify one.

The real question is whether the person holding the license understands what the license allows them to do.

An agent is not an attorney. An agent should not give legal advice. But agents do fill out contracts, explain process, identify risks, coordinate timelines, communicate material facts, and guide clients through decisions. That work requires a higher level of seriousness than the industry sometimes admits.

The Opposing View on Age: Raising the Minimum to 21 Could Block Opportunity

The strongest argument against a 21-year-old licensing minimum is that it could block talented young people from entering the profession.

That matters. Real estate can be one of the few entrepreneurial industries where someone without a college degree can enter, learn, work hard, and build a business. Increasing barriers can reduce opportunity, especially for young workers, women, and people without family wealth.

Research by Samuel J. Ingram and Aaron Yelowitz found that increased real estate licensing stringency reduced labor-market entry response by 30%, with stronger impacts on women and younger workers, based on analysis of 100 large U.S. metro areas from 2012 to 2017 (Journal of Entrepreneurship and Public Policy via RePEc). That does not automatically mean every licensing requirement is bad, but it does show that raising barriers has consequences.

The counterargument says the industry should not solve professionalism problems by shutting out young people. It should solve them through better supervision, better broker accountability, stronger apprenticeship models, contract-writing training, mentorship, and continuing education.

That view deserves respect.

But here is my answer: if the industry wants to keep the licensing age at 18, then it needs to make supervision real. Not theoretical. Not “call me if you need anything.” Real supervision. Real contract review. Real mentorship. Real accountability for brokers who activate new agents and then leave them alone.

If we are going to let 18-year-olds handle contracts, then the supervising broker’s responsibility must be serious enough to match the risk.

What I Would Change

Here is the standard I believe the industry should move toward.

First, the minimum age for a real estate salesperson license should be 21. The role carries too much legal and financial responsibility to treat it like a low-risk sales job.

Second, if a state keeps the age at 18, new licensees under 21 should be required to complete a structured apprenticeship period before independently writing offers or managing contracts. That apprenticeship should include broker review, transaction shadowing, contract workshops, and documented competency sign-offs.

Third, every licensing exam should test real contract comprehension. Not just vocabulary. Not just “what does escrow mean?” The exam should test whether the applicant can read a realistic contract clause, identify the deadline, understand who has the right to cancel, and explain the consequence.

Fourth, bilingual service should be encouraged, not punished. Spanish-speaking consumers deserve Spanish-speaking professionals. But if the contract is in English, the agent’s license should prove English contract literacy.

Fifth, real estate schools should teach language access as a professional responsibility. Agents should learn when to use interpreters, when to use translated resources, when to document language support, and how to avoid misrepresenting English legal documents.

Sixth, brokers should be held more accountable for who they sponsor. The sponsoring broker should not be a name on a form. The broker is the safety net between a new licensee and a consumer who may not know enough to recognize bad guidance. ** This Is About Respecting the Consumer**

The real estate industry talks constantly about professionalism. But professionalism is not a slogan. It is not a headshot. It is not a luxury logo. It is not a social media bio. Professionalism is the willingness to hold the license to the weight of what it represents.

Consumers are trusting agents with homes, money, debt, family decisions, school districts, retirement plans, divorce transitions, estate sales, relocations, military moves, investments, and sometimes the only major asset they will ever own.

That deserves a higher standard.

You should not have to own a home to sell one. But you should have to understand the process so deeply that your client is safer because you are in the room.

You should not have to speak only English to serve in real estate. But if the legal contract is written in English, you should be able to read it, understand it, and know when your client needs qualified translation support.

You should not have to be old to be professional. But the license should reflect the seriousness of the work. If 21 is too high for some people, then the alternative cannot be business as usual. The alternative has to be real training, real supervision, and real accountability.

The point is not to make it harder for good people to enter real estate. The point is to make it harder for unprepared people to harm consumers.

Key Takeaway

The real estate industry does not need a homeownership requirement. It needs a competence requirement. Ownership is personal experience. Competence is professional responsibility.