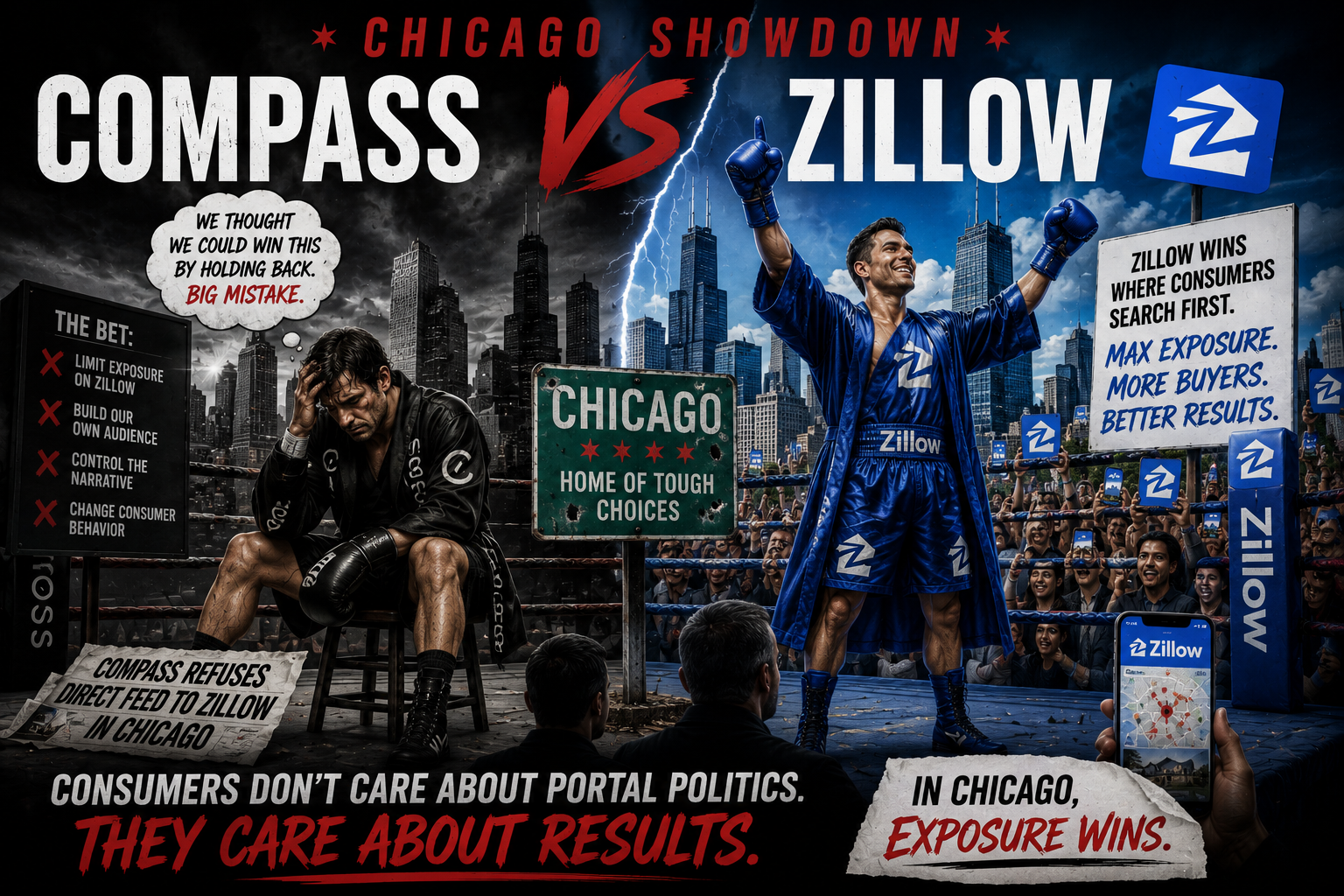

A fascinating battle is quietly unfolding in Chicago.

And while it may appear on the surface to be a dispute about listing feeds and portal strategy, the implications are much bigger than that.

At the center of the conflict is a deceptively simple question:

Who actually owns consumer behavior in real estate?

Compass appears to be betting that brokerages with enough inventory and agent influence can begin reclaiming power from portals like Zillow by limiting listing distribution and pushing consumers directly into brokerage-controlled ecosystems.

Meanwhile, Zillow is betting on something entirely different:

That consumer search behavior is already permanently ingrained — and no brokerage, regardless of size, can realistically change it at scale.

This is not just a technology disagreement.

It is a battle over leverage.

And Chicago may become the first major test case revealing who truly has more power:

the brokerage…or the platform.

The loser here, if it’s Compass, may lose more than the battle itself. They may lose the consumers' trust. (More on this later)

Compass Is Challenging the Existing Distribution Model

For years, the relationship between brokerages and Zillow was relatively straightforward.

Brokerages provided listings.

Zillow provided exposure.

In many ways, the industry accepted this arrangement because it benefited everyone:

- sellers received visibility,

- buyers gained convenience,

- and agents gained lead opportunities.

- not to mention that fact that the national MLS’s sold agents and brokerages out

But over time, many brokerages began feeling an uncomfortable shift.

The platforms distributing the listings were becoming more powerful than the companies creating them.

That tension has been building quietly for years.

Now Compass appears willing to challenge it more aggressively than most.

While many brokerages continue supplying listings through direct feeds, Compass has reportedly doubled down in certain markets by resisting participation and attempting to strengthen its own ecosystem and consumer pathways instead.

Strategically, the logic is understandable.

If brokerages continue handing over their most valuable asset - inventory - they may continue reinforcing the very platforms competing for consumer attention, agent relationships, and long-term industry influence.

From that perspective, Compass is not simply protecting listings.

It is attempting to reclaim distribution power.

Did the MLS Industry Quietly Help Create Zillow’s Dominance?

This is the uncomfortable question many agents and brokers have asked privately for years.

Because Zillow did not become dominant simply through brilliant marketing alone.

The industry itself helped build the machine.

For years, MLS organizations and data providers across the country supplied listing data directly into the portal ecosystem, helping create the most comprehensive and convenient consumer search experience ever assembled in real estate. Ultimately they helped create the industry's biggest competitor.

At the time, the logic made sense:

- more exposure,

- broader reach,

- easier consumer access,

- and more online visibility.

But in hindsight, many brokers now feel the industry underestimated the long-term consequences.

Because once listing data became centralized at massive scale, Zillow gained something far more valuable than listings themselves:

Consumer habit.

The industry effectively trained consumers to begin their home search on Zillow.

And once that behavioral loop was established nationally, the balance of power shifted permanently.

Many brokerage leaders now quietly wonder whether the MLS system unintentionally helped create the very platform dominance brokerages are struggling against today.

Because while brokers technically still own the listings…

the portals increasingly own the audience.

And in modern business, audience ownership is often the more powerful asset.

But Consumer Habits Are Extremely Difficult to Break

The problem is that consumer behavior may already be far more entrenched than many brokerages want to admit.

And nowhere is that more obvious than with Zillow.

Consumers do not use Zillow because of brokerage loyalty.

They use Zillow because:

- it’s familiar,

- convenient,

- widely trusted,

- and already embedded into consumer behavior patterns.

That matters enormously.

Because changing consumer behavior is one of the hardest things any company can attempt.

Especially at the national scale.

The average buyer is not thinking about:

- brokerage economics,

- listing syndication politics,

- or portal power dynamics.

They simply want the easiest and most complete home search experience possible.

And currently, Zillow still overwhelmingly owns that position in the consumer’s mind.

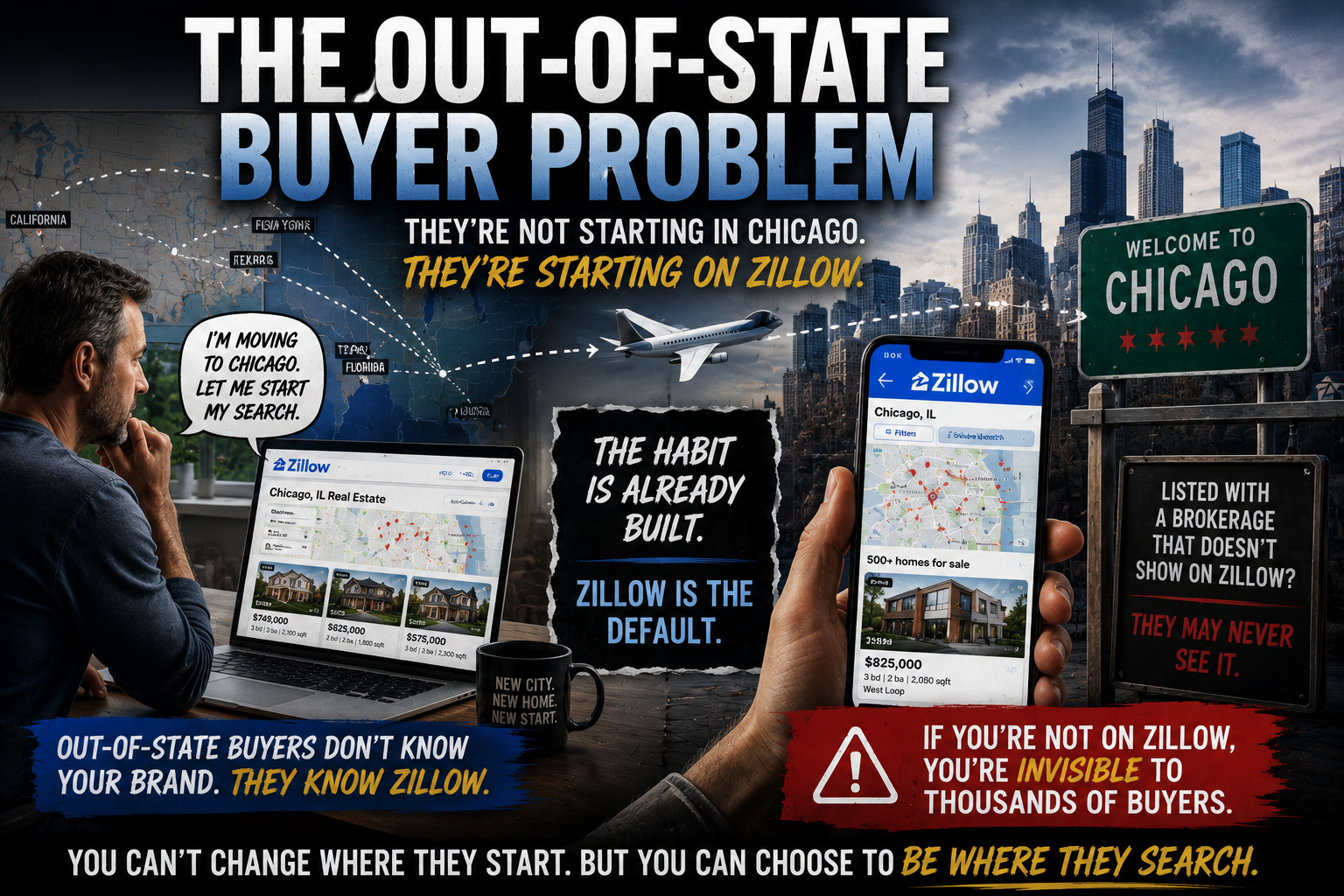

The Out-of-State Buyer Problem

This is where the Compass strategy becomes particularly vulnerable.

Even if local Chicago consumers gradually adapt to alternative search behaviors, out-of-state buyers likely will not.

And in many markets ,especially major cities - out-of-state demand matters significantly.

A relocating buyer from:

- California,

- Texas,

- Florida,

- New York,

- or overseas…

Is almost certainly beginning their search on Zillow, not on a local brokerage website.

Why would they change?

There is currently very little incentive for them to do so.

Most consumers are not emotionally invested in brokerage brands.

They are invested in convenience.

That creates a major challenge for any brokerage attempting to reduce Zillow exposure:

you are not just fighting a technology platform.

You are fighting consumer habit formation at national scale.

That is an extraordinarily difficult battle to win.

The Bigger Risk May Be to Sellers

And this leads to the most important question in the entire debate:

Why would a seller willingly reduce exposure?

Because regardless of industry politics, sellers generally want one thing above all else:

Maximum visibility.

Most homeowners are not deeply concerned with whether:

- Zillow gains traffic,

- brokerages gain leverage,

- or portals gain power.

They care about:

- getting the highest possible price,

- generating the most buyer demand,

- and maximizing competition.

That creates a potentially uncomfortable conversation for agents.

If Zillow still represents one of the largest pools of consumer traffic in real estate, then sellers may naturally begin asking:

Why would I intentionally limit exposure to the largest audience of buyers?

Especially when many sellers already perceive Zillow visibility as synonymous with market visibility itself.

That perception may or may not be fully accurate… but perception often matters more than technical reality.

There May Actually Be Three Types of Brokerages Emerging

Most people frame this battle as:

- portals versus brokerages,

- or technology platforms versus traditional real estate companies.

But the reality may be more nuanced.

There may actually be three different brokerage philosophies emerging.

1. Brokerages Trying to Reclaim Control

These companies believe brokerages surrendered too much leverage to portals and are now trying to rebuild direct consumer relationships.

This is where Compass largely fits.

2. Brokerages Fully Embracing Platform Distribution

These companies believe maximum exposure matters most and view portals like Zillow as essential consumer infrastructure.

For them, broad syndication is simply good business.

3. Consumer-First Brokerages

And then there is a third category emerging quietly in the middle.

These brokerages are less focused on “winning” against portals and more focused on supporting consumers however consumers most want to be served.

And if consumers overwhelmingly prefer Zillow…

then these brokerages will support that behavior rather than fight it.

Their philosophy is simple:

The consumer ultimately decides the platform.

Not the brokerage.

These companies may believe the real competitive advantage is not controlling search traffic…

but providing exceptional service regardless of where the consumer originates.

That is a very different strategic mindset.

And honestly, it may prove to be the most sustainable one long term.

This Is Really a Battle Over Dependency

Underneath all of this lies a much bigger industry fear:

Brokerages increasingly worry they have become too dependent on platforms they do not control.

And frankly, that concern is understandable.

Over time, portals evolved from:

- advertising platforms,

- into lead platforms,

- into consumer platforms,

- into increasingly influential industry gatekeepers.

That evolution has fundamentally shifted power away from traditional brokerages.

The companies creating the inventory no longer fully control the consumer relationship surrounding that inventory.

That reality frustrates many brokerage leaders. But other Brokerages have the unique skill to lean into these platforms as a way to support their agents and team leaders.

And Compass may simply be the first major company willing to push back aggressively enough to test the limits.

But Zillow May Already Have Won the Consumer Layer

The uncomfortable possibility for brokerages is this:

The portal war may have already been decided years ago.

Not contractually.

Psychologically.

Consumers now instinctively search for homes the same way they:

- search on Google,

- shop on Amazon,

- or watch content on YouTube.

The platform itself becomes the default behavior.

Once that happens, reversing the habit becomes incredibly difficult.

Even if brokerages technically possess the inventory.

Because inventory ownership alone does not guarantee consumer attention anymore.

Distribution does.

And Zillow spent years building distribution at enormous scale.

The Industry Is Quietly Divided on This

What makes this showdown particularly fascinating is that many brokerage leaders likely agree with Compass philosophically…

while simultaneously doubting whether consumers will ever truly follow.

That creates an industry contradiction.

Brokerages want:

- more control,

- less dependency,

- and stronger direct consumer relationships.

But consumers continue rewarding:

- simplicity,

- familiarity,

- and centralized search behavior.

Those two realities are now colliding in real time.

Chicago may simply be where the collision becomes visible first.

The Outcome Could Reshape Brokerage Strategy Nationally

If Compass succeeds in proving that:

- consumers will follow brokerage ecosystems,

- sellers will tolerate reduced Zillow exposure,

- and agents can maintain competitive advantage independently…

then the entire industry may rethink portal relationships over the next decade.

But if consumer behavior remains unchanged…

and sellers increasingly demand maximum portal exposure…

then this experiment may ultimately reinforce Zillow’s dominance even further.

Because the real power in modern real estate may no longer belong to whoever controls the listings.

It may belong to whoever controls consumer attention.

And those are not always the same thing.

The Most Interesting Part of the Entire Debate

Ironically, both sides may be right.

Compass is likely correct that brokerages surrendered too much long-term leverage to portals.

But Zillow may also be correct that consumer behavior has already evolved beyond brokerage control.

That is what makes this battle so important.

This is no longer simply a disagreement about listing feeds.

It is a referendum on whether brokerages still possess enough influence to reshape how consumers search for homes in the first place.

And the answer to that question could define the next era of real estate.

The Contrarian View: What If Compass Is Actually the One Taking the Bigger Risk?

Most of the industry discussion surrounding the Chicago showdown has focused on whether Zillow is too powerful.

But there is another possibility that deserves serious attention:

What if Compass is the side most vulnerable here?

Because while the anti-portal argument is intellectually compelling, the market ultimately does not reward philosophy.

It rewards consumer behavior.

And consumers have repeatedly shown that they overwhelmingly value:

- convenience,

- visibility,

- and maximum exposure.

That creates a potentially dangerous position for Compass if sellers begin viewing reduced Zillow exposure not as strategic…

but as a liability.

Sellers Do Not Care About Portal Politics

This is the harsh reality brokerages sometimes struggle to accept.

Most consumers are not emotionally invested in the brokerage-versus-portal war.

They are not thinking about:

- listing feed control,

- platform dependency,

- or long-term brokerage leverage.

They are thinking about:

“How do I get the most money for my home?”

And in the mind of many consumers, maximum exposure equals maximum opportunity.

Whether that perception is technically correct is almost irrelevant.

Perception itself shapes behavior.

Which means if sellers begin believing:

“My home gets less visibility without Zillow”…

then many may simply avoid the brokerage creating that limitation.

That is the real risk Compass may be underestimating.

Consumers Rarely Move Backward on Convenience

History shows consumers almost never willingly move backward in convenience once habits become established.

People do not:

- stop using Amazon to shop online,

- stop using Google to search,

- or stop using YouTube to watch video content…

because individual companies object to the platform’s dominance.

The convenience layer usually wins.

And Zillow has spent years cementing itself into consumer behavior at national scale.

For many buyers, “searching for homes” and “using Zillow” have become psychologically interchangeable.

That is an incredibly difficult position to disrupt.

Especially when competing against consumer inertia itself.

Compass May Be Asking Consumers to Care About Something They Don’t Care About

This may be the core strategic problem.

Compass is framing the issue around:

- brokerage control,

- listing ownership,

- and industry leverage.

But consumers may not view the situation through that lens at all. The average seller likely asks a much simpler question:

“Will fewer buyers see my property?”

If the answer is perceived to be “yes,” then the rest of the strategic argument may collapse immediately at the consumer level.

Because no matter how intelligent the brokerage thesis may be, sellers are unlikely to prioritize industry philosophy over perceived exposure.

And that creates the possibility that consumers themselves become the force pushing brokerages back toward Zillow distribution.

The Risk Is That Compass Accidentally Strengthens Zillow Further

Ironically, the strategy designed to weaken Zillow could potentially reinforce Zillow’s importance even more.

Because if:

- consumers complain about reduced visibility,

- agents struggle explaining the strategy,

- or listings appear harder to find…

then Zillow’s value proposition becomes even clearer in the consumer’s mind.

The portal stops looking optional.

It starts looking essential.

And once consumers begin demanding Zillow presence directly from agents, brokerages may lose negotiating leverage entirely.

At that point, the market effectively chooses the platform for them.

The Most Dangerous Outcome for Compass

The biggest risk may not be losing agents.

It may be losing consumer trust.

Because if sellers begin associating Compass with:

- reduced exposure,

- smaller buyer pools,

- or limited distribution…

that perception could become incredibly difficult to reverse.

Especially in a competitive listing environment where agents from other brokerages can simply say:

“We put your property everywhere buyers are already searching.”

That is a very easy consumer message to understand.

And simplicity usually wins.

This Is What Makes the Chicago Battle So Important

The Chicago showdown matters because it may answer a much larger question for the entire industry:

Can brokerages still shape consumer behavior…

or has consumer behavior already become stronger than brokerage influence itself?

If Compass succeeds, brokerages across the country may begin reclaiming leverage from portals.

But if consumers reject the strategy and continue demanding Zillow exposure, the opposite may happen:

The industry could become even more dependent on portals than it already is today.

And that outcome may permanently settle the debate over who truly owns the consumer relationship in real estate.